Your Family Financial Bill of Rights

- Dec 20, 2025

- 4 min read

A framework for raising financially capable adults

Most families have unspoken rules about money. “Money causes fights.” “We don’t talk about debt at dinner.” “Dad handles investments; Mom handles groceries.” “Rich people are the enemy.”

The problem with unspoken rules is that kids learn by observation, often picking up on the anxiety rather than the strategy.

If we want to raise financially capable adults, we need to explicitly state the values that govern our household economy. We need a Family Financial Bill of Rights.

Here is a template to start yours. These aren't just rules for the kids—they are commitments from the parents to the family unit.

1. The Right to Curiosity

Money isn't a dirty secret. We err on the side of openness. While we introduce concepts appropriately by age, our goal is full transparency—including household cashflows—once the kids have the maturity to understand the context. No question is off-limits. We promise to answer questions about costs, salaries, or lifestyle comparisons with context and honesty, rather than shutting them down with, "That's none of your business." We normalize the conversation so money talk never feels taboo.

2. The Right to a Voice

Financial decisions involve tradeoffs. Every family member has the right to weigh in on key decisions. While we have final say on how discretionary family funds are spent; we invite opinions. "Would you rather have two smaller camping trips this year, or save up for one big theme park trip?" Learning to budget, weigh options, and make informed decisions is a critical financial skill.

3. The Right to Align Money with Values

We recognize that price does not equal value. We prioritize safety and quality over frugality, but we also thrift and participate in gift economies. Having the money is not a license to purchase things that misalign with our family values. Our spending is a reflection of who we are. Just because we can buy something doesn't mean we will. We will set spending guardrails for our kids both to align with our family values and to promote their health and safety.

4. The Right to Own Discretionary Spending

We draw a hard line on funding discretionary wants. While we provide a weekly allowance and stipends for specific needs (plus generous gifts on birthdays and year end holidays), our kids may not add discretionary items to our shopping cart. If they want "extras," they come out of their budget, not ours. Furthermore, they must have the money before spending it (no childhood debt). These clear boundaries teach prioritization better than any lecture.

5. The Right to Make Mistakes (Safely)

The stakes are low when kids are 10; they are high when they are 25. We believe children have the right to spend their own money on things they care about, regardless of the value we place on these items (e.g., cheap plastic toys, trading cards, or in-game credits). When they run out of money and experience "bankruptcy," we celebrate the lesson rather than bailing them out. We let our children feel the sting of going broke, then support them as they problem-solve their way out of the hole.

6. The Right to Earn

In this house, money is not an entitlement; it is an exchange of value. We provide for our children’s needs with love and devotion, and we accommodate wants out of benevolence, not obligation. We do not owe our children brand-name sneakers, the latest iPhone, or sushi dinners; these are luxuries, not rights. While family membership includes responsibilities (unpaid Family Roles), our children have the right to earn money inside and outside the home for these extras. They do so by solving problems and adding value above and beyond their basic duties.

7. The Right to Future Security (For Everyone)

We prioritize the financial health of the household over short-term wants. This isn't just for us parents; we require our children to save a portion of every dollar they earn, no matter how much they protest. We enforce this not to be controlling, but to build the muscle of discipline. Their future selves will be grateful—not just for the nest egg, but for the habits that built it.

How to use this Family Financial Bill of Rights:

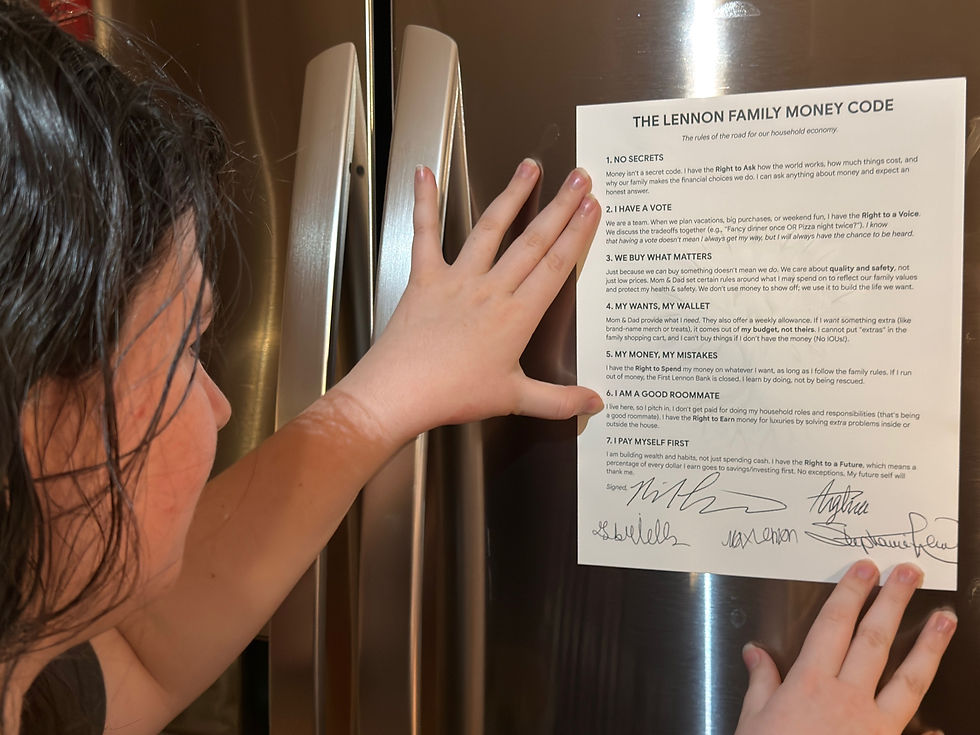

1. The "Fridge Test" (Downloadable)

This article is the strategic framework for you (the parents). But your 12-year-old isn't going to read a manifesto. I’ve created a simplified, "Kid-Friendly Money Code" that translates these values into a one-page poster.

Copy the "Family Money Code" poster here

Edit it to align with your family’s priorities

Print it, have everyone sign it, and post it on the fridge. It shifts the conversation from "Because I said so" to "Because we signed the code."

2. Join the Conversation

Which of these "Rights" makes you the most nervous? Is it Transparency (telling kids what you make) or letting them make Mistakes (watching them waste money)? Drop a comment below—I’d love to hear which rule feels hardest to implement.

3. Break the Ice Tonight

Posting the code is step one. Actually talking about it is step two. If you need help starting the conversation without it feeling awkward, download these Free Dinner Table Discussion Starters. It’s a list of questions designed to get your kids talking about money values without the lecture.

Stephanie Lennon is the author of Family Bank Blueprint, GoldQuest, and What Would Water Do? Simple Strategies for Navigating Life's Obstacles. Her titles are available in Paperback and Kindle on Amazon.com.

Comments